Research Article - (2023) Volume 20, Issue 3

Inequalities in Willingness to Pay for Zambia’s National Health Insurance Scheme

Mulenga Kabaso* and

Frederik Booysen

Department of Health Economics and Policy Association, University of the Witwatersrand, Johannesburg, South Africa

*Correspondence:

Mulenga Kabaso, Department of Health Economics and Policy Association, University of the Witwatersrand, Johannesburg,

South Africa,

Email:

Received: 24-Nov-2022, Manuscript No. IPDEHC-22-14960;

Editor assigned: 28-Nov-2022, Pre QC No. IPDEHC-22-14960 (PQ);

Reviewed: 12-Dec-2022, QC No. IPDEHC-22-14960;

Revised: 24-Feb-2023, Manuscript No. IPDEHC-22-14960 (R);

Published:

03-Mar-2023, DOI: 10.21767/2049-5471.20.3.011

Abstract

This paper investigates socioeconomic inequalities in household willingness to pay for national health

Insurance. The paper used data from the nationally representative Zambia household health

expenditure and utilization survey. Contingent valuation was used to elicit willingness to pay using a

bidding game technique. A concentration curve and a concentration index were used to measure

inequalities in willingness to pay, while Wagstaff, et al. decomposition was used to identify the factors

that contribute to these inequalities. The concentration index for socioeconomic inequalities in

willingness to pay was estimated at 0.161, indicating that willingness to pay was concentrated among

affluent households. The Wagstaff, et al. decomposition results suggested that the ability to pay,

proxied by per capita expenditure, contributed most to the inequalities in willingness to pay.

Thus, policy makers should target programs that create employment and income generating

activities that absorb everyone regardless of their socioeconomic status.

Keywords

Willingness to pay; Socio-economic inequality; Concentration index; Decomposition;

Zambia

Introduction

Universal Health Coverage (UHC) is a global health policy

agenda that has been adopted as one of the health targets of

Sustainable Development Goal (SDG) number 3, which is to

ensure healthy lives and promote wellbeing for all ages

(World Health Organization, 2015). This target states that we

should “achieve UHC, including financial protection, access to

quality essential healthcare services and access to safe,

effective, quality and affordable essential medicines and

vaccines for all”. Consequently, a predictable and sustainable health financing mechanism is therefore pivotal to health

system reform if UHC is to be attained.

To this effect, the government of Zambia is in the process of

implementing a mandatory national health insurance scheme.

This is to avoid high costs people incur when seeking health

care. The purpose of the scheme is to ensure that everyone

starts paying in advance for future health care expenditures

instead of having to pay when they are sick. A national health

insurance scheme will offer people health care when they

need it and protect them from high health expenditures and

risks of being impoverished due to ill health and emergency

health expenditures. The scheme will also assist in ensuring sustainable, predictable and dedicated financing for the

health sector whilst at the same time providing financial risk

protection for its citizenry.

In Zambia, such financing mechanism could be an important

way for improving health care utilization and improving health

status. Some of the major problems facing the health sector in

the country include limited funds for healthcare, elevated

disease burden especially in this advent of HIV/AIDS and

COVID-19, staff shortages, low and inequitable utilization and

poor quality health services. These problems prevent health

care from having a notable impact on health. The national

health insurance scheme will provide additional funding to

the Zambian health sector along with tax financing, private

health insurance and community based insurance.

Only a single study on willingness to pay for health insurance

explored inequalities in willingness to pay. Dong, et

al., documented inequalities in willingness to pay for

Community Based Insurance (CBI) by expenditure quintile

using data collected from a household survey in Burkina

Faso. A bidding game method of contingent evaluation

was used to elicit willingness to pay. The results from

study show that the poorer people were willing to pay

less for CBI. Dong, et al., study further stated that,

households might be a better unit of enrolment in terms of

equity than the individual, since the distribution of

willingness to pay by household was less unequal than

the distribution of willingness to pay by individuals.

Unlike Dong, et al., study this paper adds to literature

by not only documenting socioeconomic inequalities

in household willingness to pay for national health

insurance in Zambia but also decomposing the factors that

contribute to the socioeconomic inequalities. Doing so will

help policy makers with the levers with which to address

inequalities in willingness to pay for the scheme [1-7].

Theoretical Framework

The conceptual framework discusses the way the analysis is

modeled and the reasons behind the choice of models, in line

with the literature review. The model specification is based on

the neoclassical theory of welfare economics that assumes

that households are rational. Households aim to maximize

their utility or satisfaction from consumption of any given

good, subject to their budget constraint. However, unlike in

the market for consumer goods, demand for health products

is derived demand. Implying that health is demanded not just

for its sake but to enable households to carry out certain

rewarding activities. In line with welfare economic theory

defined above, this study defines willingness to pay as the

maximum amount that a Zambian household is willing to pay

to participate in the national health insurance scheme (Figure

1).

Figure 1: Willingness to pay for how much a household values

health an improvement.

To illustrate household willingness to pay for the scheme as a

health improvement strategy, assume that household utility U

(∙) depends on income Mi. Assume further that the

introduction of national health insurance improves health

status of a household from H0 to H1. The willingness to pay for

national health insurance is thus defined as:

U (M-Y, P, H1)=U (M, P, H0 ) (1)

Where Y is willingness to pay and P is the price of non-health

goods. Therefore, willingness to pay is the amount of money

that if paid keeps the household at the initial level of utility. Figure 1 illustrates the concept of willingness to pay for

national health insurance. The two curves U0 and U1 show

how utility increases with income at two different health

states H0 and H1. To estimate a household’s maximum

willingness to pay for national health insurance, start with the

initial level of health status H0 and an income of M0 and a

utility level U*. Next determine the lower income M1 on an

improved health status H1 that results in the same utility level

U* as income M0 in the original health state H0. Willingness to

pay is the difference between M0 and M1. Thus, willingness to

pay is a measure of how much the household values

a particular improvement in health [8-12].

Materials and Methods

Data

This paper used secondary data from the 2014 Zambia

Household Health Expenditure and Utilization Survey

(ZHHEUS). The central statistical office with the support from

the ministry of health and the university of Zambia conducted

the survey to inform the national health accounts estimation

and the development of the healthcare financing strategy.

Using a two stage stratified sampling approach, it covered a

total of 12000 households, including some 59,500 individuals,

in all provinces and districts of the country.

Eliciting Willingness to Pay

Within the questionnaire, the bidding game version of

contingent valuation was used to estimate willingness to pay

for household head and other members of the family. Nine

iterations were used in the bidding game and the starting bid

was K3 000 per month, followed by the bids K2000, K1000,

K500, K300, K100, K50, K20 and then K10. The final bid question is a binary response question that indicates if the

respondent is willing to pay less than K10 per month or not.

This study mainly distinguished respondents who were willing

to pay for the scheme from those that were not willing to pay

at all.

Outcome Variable

The health outcome studied was willingness to pay, a binary

variable. The English translation of the relevant survey

question was: “Are you willing to pay for national health

insurance scheme?”

Socioeconomic Rank

Per capita expenditure was used as the measure of

socioeconomic status. Ekman explains that in situations with reliable income statistics and a large section of the population

in salaried work, socioeconomic status would be measured by

the reported income from labour and capital. But in settings,

such as those of most low-income countries, expenditure is

taken as that measure. The use of per capita expenditure as a

choice of socioeconomic status is necessitated by the

relatively large sections of the population in unsalaried labour

and the significant seasonal variations in household

income (Table 1) [13-17].

| Variable |

Definition |

Description |

| Age |

Age of household head at last birthday |

Continuous |

| Female |

Indicate gender of household head, encoded as female=1, male=0 |

Dichotomous |

| Marital status |

Indicate the marital status of household head: Never married=1, married=2, cohabiting=3, separated=4, divorced=5, widowed=6. |

Categorical |

| Education |

Highest attained level of formal education by household head: 0=none; 1=low; 2=middle and 3=high |

Categorical |

| Employment status |

Indicates employment type of the household head: Unemployed=1, informal employment=2 and formal employment=3 |

Categorical |

| Religion |

Denomination of household head: 1=catholic, 2=protestant, 3=Jehovah’s witness, 4=muslim, 5=traditionalist, 6=atheist and 7=others |

Categorical |

| Household size |

Number of people in a household |

Continuous |

| Children |

Number of children below the age of 5 years in a household |

Continuous |

| Elderly |

Number of persons above the age of 65 years in the household |

Continuous |

| Urban |

Location of household: 0=rural and 1=urban |

Dichotomous |

| Visits |

Total outpatient visits by household members in the last four weeks |

Continuous |

| Days |

Total number of inpatient days by household members |

Continuous |

| Illnesses |

Indicate whether any household member suffers from a chronic illness: 0=no, 1=yes |

Dichotomous |

| Insurance |

Health Insurance coverage of a household: 1=insured, 0=uninsured |

Dichotomous |

| Per capita expenditure |

Total per capita monthly household expenditure in Kwacha |

Continuous |

Note: All individual level characteristics refer to the characteristics of the respondent that answered the questions on household willingness to pay, namely the household head.

Table 1: Description of the factors.

Factors

The following factors were used in the decomposition

analysis.

Concentration Curve and Concentration Index

Analyses on the extent of households’ socioeconomic

inequalities in willingness to pay were done in two stages. The

first stage was to use a Concentration Curve (CC) to examine

socioeconomic inequalities in willingness to pay for national

health insurance. In the second stage, a Concentration Index

(CI) was used. The standard concentration index is defined

below:

Where h is the willingness to pay for the scheme, r is the

fractional rank of a household in the expenditure score

distribution, Cov is covariance and μ represents the mean of

the willingness to pay values. Since the outcome variable is

binary, Erreyger’s corrected concentration index was used.

The index is desirable as it satisfies properties required for

bounded variables. The equation for the Erreyger index is as

follows:

CCI=4μ/(b-a)×C (3)

Where CCI is the corrected concentration index, μ is the mean

of the willingness to pay, a and b are minimum and maximum

values of willingness to pay, respectively, and C the

standardized concentration index defined in equation (2). This

study makes use of the coindex functionality in STATA to

calculate concentration index and concentration curve.

The concentration index can either be positive or negative.

The sign of the concentration index explains the relationship

that exists between willingness to pay and position in the

wealth score distribution. If the concentration index is zero, it

means that there is no inequality in the distribution of

willingness to pay by wealth and hence the concentration

curves will coincide with the line of equality. A negative value

of the concentration index is obtained if willingness to pay is

disproportionately concentrated among the poorest

households while a positive value of concentration index

suggests willingness to pay is concentrated among the richest

households. The value of the concentration index ranges

between -1 and +1 and the concentration index provides

information about the strength of the relationship. The closer

the absolute values of the concentration index to one, the

greater the level of inequality.

Decomposition Analysis

After estimating concentration index, the causes of the

socioeconomic inequalities were determined. Decomposing

socioeconomic inequalities helps to uncover specific factors

that are potentially modifiable by policy decision makers. This

was done using the Wagstaff, et al., decomposition method

proposed by Wagstaff, et al.

Wagstaff, et al., Decomposition

Wagstaff, et al., proposed an approach that identifies factors

that explain the socioeconomic inequalities in the willingness

to pay for the national health insurance scheme. Following

equation (4) below depicts the linear relationship between

willingness to pay and its determinants:

Where y is the binary outcome variable for willingness to pay,

α is a constant, β measures the relationship between each

explanatory factor (x) and the willingness to pay variable, and

ε the error term. Like the concentration indices, the

decomposition technique used for the standard

Concentration Index (CI) was modified to suit the Corrected

Concentration Index (CCI) as follows:

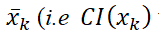

Where

Denotes the elasticity of willingness to pay to marginal

changes in the kth factor. CI (Xk) denotes the concentration

index of the kth contribution factor, while GCɛ notes the

generalized concentration index of the error term. The first

term in equation as follows:

Represents the contribution of factor k to socioeconomic

inequality in willingness to pay. It constitutes the

deterministic component of the willingness to pay

concentration index. The second term (GCε) captures the

unexplained component or the residual. The Generalised

Linear Model (GLM) with binomial family and logit link was

used to decompose the binary outcome variable. The use of

GLM with binomial distributed outcome variable and

specifying the identity link function is suitable choice in the

decomposition analysis of the binary outcome, because it

considers the structure of the distribution while preserving

the link between the regressors and dependent variables. The

contribution made by each factor is dependent on the sign

and size of the calculated elasticity and concentration index

for each factor.

All things being equal, an increase (decrease) in inequality will

increase (reduce) the degree of inequality in willingness to

pay. This study also computed bootstrapped standard errors

using 500 replications to determine whether the contribution

of each factor to socioeconomic inequality in willingness to

pay is statistically significant.

This study used the variables in Table 1 as contributing factors

in the decomposition. All categorical variables were converted

to dummies in the Wagstaff, et al., decompositions. Data

analyses were conducted in STATA software version 16.

Results

Socioeconomic and Demographic Characteristics

Table 2 shows the socio-demographic characteristics of the

households in the sample. The mean age for the household

heads is 43.3 years and the mean number of children under 5

years old in a household is about one child per household. On

average each household has 0.17 persons older than 65 years of age. Most household heads are males (75.4%) and the

majority of them are married (72.11%). The mean average

household size is 4.97 and most of the household heads only

reached a primary level of education (43%). Many of the

household heads are protestants (67.96%). Employed

household heads dominate the sample at about 78.81%, even

though most of them work in the informal sector (88.5%).

Many household heads reside in rural Zambia (58.11%)

compared to 41.89% urban. More than ninety percent of the

households (94.8%) do not have any insurance coverage. The

majority of households had no members with chronic

illnesses (60.31%), compared with those who had at least one

member with chronic illness (39.69%). The mean total

number of insured persons, the total number of outpatient

visits, the total number of inpatient days and per capita

household monthly expenditure (ZMK) are 1.25 persons, 67

visits, 1.25 days and K1,217.85 ($190.29) respectively.

| Characteristics |

Frequency |

Percentage/Mean |

Std. dev |

| Age in years |

11,743 |

43.3 |

14.98 |

| No. of children <5 years |

11,944 |

0.89 |

0.96 |

| No. of elderly >65 years |

11,944 |

0.17 |

0.43 |

| Gender |

| Male |

8,854 |

75.4 |

0.43 |

| Female |

2,891 |

24.6 |

0.43 |

| Marital status |

| Never married |

706 |

6.02 |

1.51 |

| Married |

8,467 |

72.11 |

1.51 |

| Cohabiting |

37 |

0.32 |

1.51 |

| Separated |

275 |

2.34 |

1.51 |

| Divorced |

796 |

6.78 |

1.51 |

| Widowed |

1,460 |

12.44 |

1.51 |

| Household size |

11,944 |

4.97 |

2.55 |

| Level of education |

| None |

1,183 |

10.18 |

0.83 |

| Low |

5,029 |

43.29 |

0.83 |

| Middle |

4,127 |

35.53 |

0.83 |

| High |

1,278 |

11 |

0.83 |

| Religion |

| Catholic |

2,583 |

21.99 |

0.95 |

| Protestant |

7,982 |

67.96 |

0.95 |

| Jehovah’s Witness |

766 |

6.52 |

0.95 |

| Muslim |

56 |

0.48 |

0.95 |

| Traditional |

92 |

0.78 |

0.95 |

| Atheist |

109 |

0.93 |

0.95 |

| Other |

157 |

1.34 |

0.95 |

| Employment status |

| Unemployed |

2,486 |

21.18 |

0.43 |

| Formal |

1,064 |

11.5 |

0.34 |

| Informal |

8,186 |

88.5 |

0.34 |

| Place of residence |

| Urban |

4,921 |

41.89 |

0.5 |

| Rural |

6,824 |

58.11 |

0.5 |

| Insurance |

| Insured |

624 |

5.2 |

0.24 |

| Uninsured |

11,320 |

94.8 |

0.24 |

| Illness |

| Yes |

4,741 |

39.69 |

0.39 |

| No |

7,203 |

60.31 |

0.39 |

| Total number of outpatient visits |

11,944 |

0.67 |

1.03 |

| Total number of inpatient days |

11,944 |

0.16 |

0.48 |

| Per capita monthly HH expenditure (ZMK) |

11,944 |

1,217.85 |

2,599.26 |

Note: Individual socio-demographic characteristics represent those of the household head.

Table 2: Socio-demographic and other household characteristics.

Willingness to Pay for National Health Insurance

Scheme

The data showed that there is overwhelming support for the

recently introduced national health insurance by the

government of Zambia. About 90 percent of households in

the sample rated the scheme as excellent, very good or good.

Households in the rural areas were more positive about the

scheme than urban households. Most households thought the

scheme will make health care affordable and protect them

against high health expenditures. The study found that,

majority (80%) of Zambian households was willing to pay

for the National Health Insurance scheme. The mean

national health insurance contribution to be paid monthly

was K90.76 (95% CI K84.29-K97.23) corresponding to 7.4%

of average monthly household expenditure (K1,217.85).

The median willingness to pay contribution was K10.00

implying that the 50th percentile of willingness to pay

laid at K10.00. The number of households not willing to pay for the scheme was 2,401 corresponding to 20% of all

households. Of these households, about 77% indicted that

they could not afford paying the contributions for the

scheme. About 67% of households who stated that, they

could not afford paying for the scheme were located in rural

areas and their household heads were either unemployed

or worked in the informal sector.

Concentration Curve and Concentration Index

Figure 2 below shows the concentration curve for willingness

to pay for national health insurance scheme. The curve lies

below the 45 degree line of equality, showing that willingness

to pay is concentrated among the affluent households. The CI

value of 0.161 is positive and highly significant at

conventional levels. Thus, willingness to pay for national

health insurance is concentrated among the non-poor

segments of the population. The results from the CC and CI,

therefore, indicate that willingness to pay for the scheme is higher among non-poor households. In other words, poorer

households are less willing to pay for national health

insurance scheme in Zambia.

Figure 2: Concentration curve for willingness to pay for

national health insurance.

Socioeconomic Related Inequality in Willingness to Pay

Table 3 shows that the per capita expenditure factor makes

the most statistically significant positive contribution to

inequalities in willingness to pay of about 92.212%. Thus,

reducing inequalities in households’ ability to pay which is

proxied by per capita expenditure reduces inequalities in

willingness to pay by about 92%. Equally, household size

makes the largest negative contribution to inequalities in

willingness to pay (-10.822%). This implies that eliminating

inequalities in household size will increase inequalities in

willingness to pay by about 11%.

| Factor |

Elasticity |

CI |

Absolute |

S.E |

% |

Total (%) |

| Age |

-0.067 |

-0.021 |

0.006*** |

0.001 |

3.6 |

3.6 |

| Gender |

-0.006 |

-0.045 |

0.001* |

0.001 |

0.663 |

0.663 |

| Marital status |

| Unmarried |

(base) |

(base) |

(base) |

(base) |

(base) |

|

| Married |

0.047 |

-0.025 |

-0.005*** |

0.001 |

-3.088 |

|

| Cohabiting |

0 |

0.279 |

0 |

0 |

-0.032 |

|

| Separated |

0.001 |

0.098 |

0.001 |

0 |

0.34 |

|

| Divorced |

0.002 |

-0.032 |

0 |

0 |

-0.149 |

|

| Widowed |

0.005 |

-0.067 |

-0.001 |

0.001 |

-0.883 |

|

| |

|

|

|

|

|

-3.812 |

| Religion |

| Catholic |

(base) |

(base) |

(base) |

(base) |

(base) |

|

| Protestant |

-0.019 |

-0.012 |

0.001** |

0 |

0.584 |

|

| Jehovah’s witness |

-0.002 |

0.062 |

0 |

0 |

-0.259 |

|

| Muslim |

0 |

0.22 |

0 |

0 |

0.233 |

|

| Traditionalist |

-0.001 |

-0.36 |

0.001** |

0 |

|

|

| Atheist |

-0.001 |

-0.169 |

0.001** |

0 |

0.469 |

|

| Other |

-0.001 |

-0.048 |

0 |

0 |

0.125 |

|

| |

|

|

|

|

|

1.759 |

| Urban |

-0.002 |

0.407 |

-0.003 |

0.007 |

-1.808 |

-1.808 |

| Education |

| None |

(base) |

(base) |

(base) |

(base) |

(base) |

|

| Low |

0.012 |

-0.244 |

-0.010** |

0.004 |

-6.445 |

|

| Middle |

0.022 |

0.166 |

0.014*** |

0.003 |

8.625 |

|

| High |

0.004 |

0.701 |

0.009 |

0.006 |

5.447 |

|

| |

|

|

|

|

|

7.627 |

| Insured |

-0.004 |

0.658 |

-0.012*** |

0.003 |

-7.362 |

-7.362 |

| Illness |

0.01 |

0.005 |

0 |

0 |

0.119 |

0.119 |

| Household size |

0.064 |

-0.064 |

-0.017*** |

0.003 |

-10.822 |

-10.822 |

| Children |

0.003 |

-0.16 |

-0.0019 |

0.003 |

-0.999 |

-0.999 |

| Employment status |

| Unemployment |

(base) |

(base) |

(base) |

(base) |

(base) |

|

| Formal |

0.004 |

0.571 |

0.008 *** |

0.005 |

5.249 |

|

| Informal |

0.028 |

-0.037 |

-0.004* |

0.001 |

-2.578 |

|

| |

|

|

|

|

|

2.671 |

| Elderly |

-0.008 |

-0.15 |

0.004*** |

0.001 |

2.698 |

2.698 |

| Visits |

0.001 |

-0.162 |

-0.001 |

0.002 |

-0.435 |

-0.435 |

| Total inpatient days |

0 |

-0.066 |

0 |

0 |

-0.06 |

-0.06 |

| Per capita expenditure |

| Quintile 1 |

(base) |

(base) |

(base) |

(base) |

(base) |

|

| Quintile 2 |

0.016 |

-0.4 |

-0.025*** |

0.003 |

-15.765 |

|

| Quintile 3 |

0.025 |

0 |

0.001*** |

0.001 |

0.015 |

|

| Quintile 4 |

0.026 |

0.4 |

0.041*** |

0.004 |

25.667 |

|

| Quintile 5 |

0.04 |

0.8 |

0.133*** |

0.011 |

82.295 |

|

| |

|

|

|

|

|

92.212 |

| Explained |

|

|

|

|

86.049 |

86.049 |

| Residual |

|

|

0.022** |

0.009 |

13.951 |

13.951 |

| Total |

|

|

0.161 |

|

100 |

100 |

Note: CI: Erreygers concentration index; Absolute: Absolute contribution; SE: Bootstrapped standard errors for the absolute contributions obtaineda bootstrapping method using 500 replications. *** p<0.01, ** p<0.05, * p<0.1

Table 3: Decomposition of concentration index for willingness to pay.

Other factors that made positive contributions to inequalities

in willingness to pay include age (3.6%), gender (0.66%),

religion (1.759%), education (7.627%), illness (0.119%),

employment status (2.671%), and being elderly (2.698%). All

positive contributions of variables show that reducing

inequalities in these variables reduces the degree of

inequalities in willingness to pay. Alternatively, eliminating

inequalities in the positive contributing variables lowers

inequalities in willingness to pay for Zambia’s national health

insurance scheme. The other factors that made negative

contributions to inequalities in willingness to pay include marital status (-3.812%), place of residence (-1.808%),

insurance status (-7.362%), children (0.999), visits (-0.435)

and total inpatient days (-0.06). Thus, all things being equal,

all negative contributions of the variables imply that the

elimination of inequality in these variables will increase the

degree of inequality in willingness to pay for the national

health insurance scheme.

The factors included in the paper explained about 86.049% of

the overall inequality in willingness to pay. The remaining

13.951% are due to unexplained factors (residual). The residuals are statistically not different from zero at the 1%

level. Figure 3 depicts the percentage of each contributing

factor to overall inequality in willingness to pay. The largest

contributor to the willingness to pay inequality is the ability to

pay factor.

Figure 3: Percentage contribution of each factor to

overall willingness to pay inequality.

Discussion

This study examined the socioeconomic inequalities in

household willingness to pay for national health insurance in

Zambia. Given low health insurance coverage and substantial

socioeconomic disparity in accessibility and afford-ability

of health care among Zambians, this is the first study

to undertake a comprehensive assessment of inequality

in household willingness to pay for national health

insurance scheme. Analyzing the population’s willingness to

contribute to financing the national health insurance scheme

is likely to have a positive influence on the success of its

implementation and its sustainability. This study finds that

willingness to pay for the scheme is more

concentrated among wealthy households in Zambia.

Thus, affluent households are more willing to pay for

national health insurance than poor households. Thus,

policymakers should ensure that willingness to pay is

evenly distributed among poor and affluent households.

Furthermore, this study set out to determine the

factors that contribute to socioeconomic inequalities in

willingness to pay, using Wagstaff, et al., decomposition.

Results from the Wagstaff, et al., decomposition

of the binary outcome variable showed that the ability to

pay proxied by per capita expenditure quintiles, which in

Zambia’s case remains indicative of socioeconomic status,

explains most of the inequality in willingness to pay.

Eliminating inequalities between non-poor and poor

households in the ability to pay would reduce inequalities in

willingness to pay for the national health insurance scheme.

The results also showed that eliminating inequalities in

educational attainment would reduce the inequalities in

willingness to pay. Dispatch, et al., explains that the poor

fail to access high school and college education in Zambia.

Thus, the government should not only make basic

education free but should also widen access to high

schools and especially colleges and universities. If this

problem is not addressed urgently, intergenerational

inequalities will continue, and less educated households

are unlikely to participate in health enhancing ventures such as participation in health insurance schemes.

Unemployment is another variable that is diverse in Zambia

across age, gender and location. Thus, it is no surprise that

employment status is among the variables that explain

inequalities in willingness to pay. This means equalizing the

distribution of employment status between non-poor and

poor households will reduce the willingness to pay for

national health insurance. Thus, the government should

venture into employment creation activities to reduce

inequalities in willingness to pay. The other factors that

significantly explained inequalities in willingness to pay

include age and having elderly members in the household. It

is not surprising that variables such as age and having elderly

household members showed an influence on inequalities in

willingness to pay. Older people generally have poor health

compared to young people. Ageing not only involves

biological changes but also reflects accumulated effects of

one’s exposure to external risks, such as poor diet, and can be

further influenced by social changes, such as isolation and

loss of loved ones. Hence, it is difficult to separate willingness

to pay for the scheme and age. Thus, in implementing

national health insurance scheme, age related inequalities

should take on greater urgency. The paper also alluded to the

fact that the elimination of gender disparities would eliminate

inequalities in the willingness to pay for the national health

insurance scheme. Gender shapes all aspects of health and

wellbeing, including the willingness to pay for the national

health insurance. This is embedded in socially and culturally

built restrictive gender norms that define roles and

opportunities for all people, affecting determinants of health,

risk behaviour and access to quality health services. As a

result, women lose out on income-generating opportunities

such as education and employment which may lead to them

not being willing to participate in any health insurance

scheme. Thus, gender equality should be an explicit goal for

the Zambian government for sustainable implementation of

the scheme.

Conclusion

The study examined socioeconomic inequalities in household

willingness to pay for national health insurance scheme in

Zambia. This study’s results established that socioeconomic

inequalities in willingness to pay are more concentrated

among affluent households. In addition, differences in per

capita expenditure accounted the most to socioeconomic

inequalities in willingness to pay. The study suggested

contributions adjusted for income and, use of exemptions or

subsidies to help the poor. Thus, to attain greater equity in

health, government should consider a policy of varying

contributions according to income or exemptions and

subsidies. In addition, policy makers should target policies that

increase the health insurance coverage of the uninsured

households to accelerate the global goals of financial

protection and universal health coverage.

Limitations

This study has several limitations. The first limitation concerns

the use of the bidding method of contingent valuation in

eliciting willingness to pay which has a number of potential

biases. Notable among them is the hypothetical bias. In this

study, hypothetical bias is less likely because a simple scenario

was provided to the respondents in the contingent valuation

questionnaire. In addition, the hypothetical bias was reduced

in that all the analyses were conducted only for the binary

outcome variable which is less likely to suffer from the

aforementioned bias.

The other limitation concerns the results the of the

decomposition analysis where it was stated that increases in

willingness to pay inequalities is desirable for crosssubsidization

to be possible. A problem arises in that it is

difficult to establish the optimal increase in inequality for

effective cross-subsidization. In other words, it is problematic

to make any judgment on what the optimal level of inequality

in willingness to pay for national health insurance should be.

Furthermore, this study is an observational study and,

therefore, does not imply causality of the findings. However,

despite these limitations, this study is important in that it

provides an understanding of the nature and drivers of

socioeconomic inequalities in willingness to pay for national

health insurance in Zambia.

Recommendations

The results of the paper confirmed that poor households are

willing to pay less for national health insurance scheme. This

reemphasizes the importance of households’ ability to pay in

designing good policies in the implementation of the scheme.

Thus, to effectively implement the scheme, the government of

Zambia needs to consider the economic status of households.

Contributions for the scheme can be set on a sliding scale

instead of flat rates. In addition, given that per capita

expenditure is the main factor that explain inequalities in

national health insurance, there is need to create employment

and income generating activities that absorb everyone

regardless of their economic status. Given that majority of

household heads are in the informal sector where incomes are

low, government should explore subsidization and variable

mechanisms of contribution collection from the informal

sector. These could include enrolment of microfinance loan

recipients through a partnership between the bank and

insurer, as piloted in Nigeria.

Ethical Approval

The Zambia statistical agency formerly central statistical office

under the provisions of the census and statistical act number

127 of the laws of Zambian granted ethical exemptions of this

study. In addition, no identifying information of individuals

was collected and only participants above the age of 16 years

were interviewed after giving informed consent.

Competing Interests

Authors declare that they have no competing interests.

Authors' Contributions

Both authors contributed to the design of the study, data

analysis, and drafting of the manuscript. Both authors have

reviewed and approved the final version of the manuscript.

Funding

The authors do declare that no funding was received from any

individuals or organization.

Availability of Data and Materials

The dataset can be collected from the Zambia statistical

agency offices.

References

- Bala MV, Mauskopf JA, Wood LL (1999) Willingness to pay as a measure of health benefits. Pharmacoeconomics. 15(1):9-18.

[Crossref] [Google Scholar] [PubMed]

- Chilufya C (2018) Zambia ’s national health insurance scheme. Health Press Zambia Bull. 2(4):5-16.

[Google Scholar]

- Dispatch A, Thomas N, Dryding D (2019) Zambians see progress on education despite persistent inequalities. Afrobarometer. 272:1-12.

[Google Scholar]

- Dong H, Kouyate B, Cairns J, Sauerborn R (2005) Inequality in willingness-to-pay for community-based health insurance. Health Policy. 72(2):149-156.

[Google Scholar]

- Ekman B (2007) Catastrophic health payments and health insurance: Some counterintuitive evidence from one low-income country. Health Policy. 83(3):304-313.

[Crossref] [Google Scholar] [PubMed]

- Erreygers G (2006) Beyond the Health Concentration Index: An atkinson alternative for the measurement of the socioeconomic inequality of health. Biol Sci. 37:759–765.

[Google Scholar]

- Johannesson M (1996) A note on the relationship between ex ante and expected willingness to pay for health care. Soc Sci Med. 42(3):305-311.

[Crossref] [Google Scholar] [PubMed]

- Kennedy E, Binder G, Waa KH, Tidhar T, Cini K, et al. (2020) Gender inequalities in health and wellbeing across the first two decades of life: An analysis of 40 low-income and middle-income countries in the Asia-Pacific region. Lancet Glob Health. 8(12):1473-1488.

[Crossref] [Google Scholar] [PubMed]

- Ministry of health (2015). Zambia household health expenditure and utilisation survey (Zhheus) 2014 final report. Ministry of health (Zambia), Lusaka, Zambia. 1-150.

- Mitchell RC (2013). Using surveys to value public goods. 1st ed. RFF Press, New York, USA. 1-484.

[Crossref] [Google Scholar]

- O’Donnell O, Wagstaff A, Lindelow M (2008). Analyzing health equity using household survey data. World bank publications, Washington DC, USA. 2008.

[Google Scholar]

- O’Donnell O, O’Neill S, Van Ourti T, Walsh B (2016) Conindex: Estimation of concentration indices. Stata Journal. 16(1):112-138.

[Google Scholar]

- Ogundeji YK, Akomolafe B, Ohiri K, Butawa NN (2019) Factors influencing willingness and ability to pay for social health insurance in Nigeria. PLoS ONE, 14(8):1–10.

[Crossref] [Google Scholar] [PubMed]

- Peterson A, Omasanjuwa E, Ambrose K, Hatt LLC (2015) Extending health insurance to informal sector workers in urban settings: Findings from a micro insurance pilot in Lagos, Nigeria. Health Fin Govern Proj. 1:1-35.

[Google Scholar]

- Vasoontara Y, Lim LY, Gordon LA, Keith CBG, Adrian CS (2010) Decomposing socioeconomic inequality for binary health outcomes: An improved estimation that does not vary by choice of reference group. BMC Research Notes. 3(57):1-8.

[Crossref] [Google Scholar] [PubMed]

- Wagstaff A (1986) The demand for health: Theory and aplications. J Epidemiol Community Health. 40(1):1-11.

[Crossref] [Google Scholar] [PubMed]

- Wagstaff A, Doorslaer EV (2003) Catastrophe and impoverishment in paying for health care: With applications to Vietnam 1993--1998. Health Econ. 934:921-934.

[Crossref] [Google Scholar] [PubMed]

Citation: Kabaso M, Booysen F (2023) Inequalities in Willingness to Pay for Zambia’s National Health Insurance Scheme. Divers

Equal Health Care. 20:011.

Copyright: © 2023 Kabaso M, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution

License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source

are credited.