3rd World Congress on Gastroenterology and Hepatology: Market Analysis

Vinod Nikhra

Senior Chief Medical Officer (Senior Administrative Grade), Consultant in Department of Medicine, Hindu Rao Hospital and NDMC Medical College, New Delhi, India, E-mail: drvinodnikhra@rediffmail.com

After a successful conference in 2019, Euroscicon is very

delighted to invite you all to the “3rd world congress on

gastroenterology and hepatology” (euro gastro 2020) Norway.

We are progressively working for the initiation of new world,

perspectives and views in restorative therapeutic field.

Euroscicon is providing a great platform for thousands of

gastroenterologist and hepatologist, researchers and medical

practioners meet, learn, share and exchange views. We are

concentrating on a view that everyone should gain from the

conference. So, we are organizing plenary sessions, poster

exhibitions and section programs, workshops at the

conference.

The worldwide gastrointestinal therapeutics showcase size

was esteemed at USD 51.9 billion of every 2016 and is

scheduled to grow at a worthwhile CAGR of 6.6% over the

estimate time frame. Expanding reception of biologics for

treatment of gastrointestinal sicknesses is the essential driver

of the market. As indicated by the Centers for Disease Control

and Prevention (CDC), it is evaluated that around 1-1.3 million

individuals are experiencing Inflammatory Bowel Disease (IBD)

in U.S. Commonness of Crohn's ailment and ulcerative colitis is

201 for each 100,000 grown-ups and 238 for every 100,000

grown-ups, separately.

To become familiar with this report, demand a free example

duplicate

A wide scope of new age therapeutics focuses on that

incorporate novel little particles and cell treatment are as of

now under scrutiny. These incorporate tofacitinib,

ustekinumab, mongersen, and vedolizumab. This deluge is

foreseen to be a result of high pervasiveness of

gastrointestinal infections all inclusive. Vedolizumab is rising as

a first-line biologic treatment for Crohn's illness. As of now, the

U.S. FDA has endorsed Humira, Amjevita, Cimzia, Remicade,

Renflexis, Inflectra, Tysabri, and Entyvio for the treatment of

Crohn's infection.

A few examinations have demonstrated that biologics

display more prominent long haul productivity. As per an

investigation led by University of Chicago, utilization of

biologics has brought about a general abatement in the

quantity of medical procedures by roughly 40.0%, crisis room

visits by 60.0%, and hospitalizations by 50.0%.

Likewise, the National Institute did an investigation on

adequacy of infliximab in treatment for Health Research and it

was accounted for to be a savvy arrangement in roundabout

treatment of dynamic Crohn's Disease. Expanding requirement

for cost regulation in sedate improvement just as organization

costs is probably going to fuel development open doors for

biologics. Coming of focused treatment options has prompted

improvement of progressively customized biologics.

Type Insights

Marked gastrointestinal medications held the prevailing

offer side-effect in 2016. Be that as it may, it is relied upon to

observe a decrease in CAGR all through the estimate time

frame. This decrease can be credited to expanding infiltration

of generics in the market, bringing about deals disintegration

of driving brands and less novel item dispatches. A portion of

the high income producing drugs in gastrointestinal

therapeutics that is scheduled to lapse sooner rather than

later are Emend, Sandostatin, Humira, Linzess, and Aloxi. This

is foreseen to limit development of marked medications.

Besides, patients experiencing intense gastrointestinal

bacterial diseases, recently treated with anti-microbial, are

reluctant to receive new treatment regimens. Also, increment

in multidrug-safe strains represents a test during treatment,

which is relied upon to block the development of marked

medications.

The nonexclusive section is required to develop at an

exponential rate all through the conjecture time frame

attributable to predictable expiries of licenses, cost-viability of

generics, and activities by government associations for

advancing use of generics in rising economies. Likewise,

significant pharmaceutical organizations are reliably

endeavoring to dispatch conventional forms of their marked

partners to recoup misfortunes brought about by patent lapse.

Marked medication makers and nonexclusive delivering

firms are teaming up for creating conventional medications

after patent expiry, which is required to help the development

of generics. Also, significant firms are progressively

concentrating on creating generics inferable from increment in

off-protected medications in the market. Be that as it may,

advertising selectiveness given by the FDA to patent holders for various signs is foreseen to ruin showcase development to

a slight degree.

Route of Administration Insights

In 2016, intravenous represented the predominant offer

based on course of organization. The significant offer is

foreseen to be a consequence of advantages related with IV

items. It can likewise be credited to significant expense of IV

items when contrasted with oral items. Such items incorporate

Humira, Sandostatin, Aldurazyme, Elelyso, Naglazyme,

Myozyme, Vimizim, Donnatal, Pamine, Aloxi, Pepcid AC,

Remicade, Tysabri, Entyvio, and Remsima.

As far as volume, oral items represented the biggest offer; in

any case, as far as income, the intravenous fragment

represents the predominant offer. Advantages, for example,

simplicity of organization and long haul cost effectiveness are

central point energizing the selection of these items

throughout the years.

Oral items represented the second-biggest offer in the

market for gastrointestinal therapeutics in 2016. This is an

outcome of high adequacy of oral gastrointestinal specialists

because of direct contact with influenced territories.

Nonetheless, different courses, for example, intravenous and

transdermal have more noteworthy bioavailability in contrast

with oral items, which may bring about extensive diminishing

popular. What's more, oral items are not seen as advantageous

for patients in more youthful age gatherings. In addition, there

is a more noteworthy likelihood of contraindication and lethal

medication collaborations in the event of patients

experiencing gastrointestinal malignancy treatment.

Application Insights

The others portion represented the biggest offer by

application in 2016. This section incorporates narcotic

instigated blockage, interminable idiopathic stoppage, loose

bowels, intermittent gastrointestinal contaminations, sickness,

gastrointestinal stromal tumor, pancreatic deficiency, and

touchy entrails disorder. The considerable offer can be

ascribed to a wide scope of uses for which gastrointestinal

medications have been utilized reliably over the earlier years.

Visit number of medication dispatches is likewise liable for

expanded degree for development.

Ulcerative colitis represented the second-biggest offer in the

gastrointestinal therapeutics showcase in 2016. Development

of this section can be credited to simple accessibility of

medications to treat this condition. The section is additionally

foreseen to develop at an impressive rate inferable from high

clinical direness to check developing pervasiveness of

ulcerative colitis. This high predominance is because of poor

visualization and utilization of undesirable nourishment, which

may bring about high likelihood of infection repeat.

The Crohn's infection portion is foreseen to observe a

rewarding development rate all through the conjecture time

frame. Rising pervasiveness of way of life instigated conditions, for example, unnecessary drinking and high occurrence of

incessant ailments, for example, malignancy and diabetes, are

significant development rendering drivers. As indicated by the

CDC, around 1.0-1.3 million individuals are experiencing

Inflammatory Bowel Disease (IBD). In U.S., predominance of

Crohn's ailment is 201 for each 100,000 grown-ups.

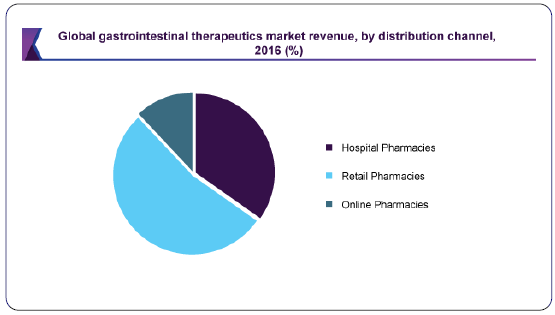

Distribution Channel Insights

In 2016, retail drug store represented the prevailing offer

regarding dispersion channel attributable to high

reasonableness and availability to retail locations. As number

of doctor prescribed prescriptions being repaid is expanding, it

is urging patients to buy drugs from retail drug stores. Retail

drug specialists likewise prescribe sedate substitutes that

anticipate antagonistic medication collaborations.

These components are probably going to support client

tendency toward retail locations. In the event that retail drug

specialists have any worries with respect to endorsed

prescriptions, they prescribe choices for the equivalent,

accordingly guaranteeing higher wellbeing. Approach of drug

store chains, for example, CVS Health is a significant supporter

of the portion of the retail section. Appropriation of digitalized

frameworks in retail drug stores to decrease danger of

blunders in remedies is likewise foreseen to fuel development

over the coming years.

Online drug stores are relied upon to show worthwhile

development during the figure time frame. This development

is foreseen to be an outcome of related advantages, for

example, high accommodation for out of commission patients

who think that it’s hard to buy drugs from medical clinics or

retail locations. What's more, developing frequency of

interminable infections has brought about a wide hole in the

stock of and interest for significant medications. The

previously mentioned elements are required to introduce

gainful development possibilities for online drug stores during

the conjecture time frame.

With the appearance of online drug stores, following and

request obtainment have gotten advantageous. Production

network Management (SCM) in online drug stores empowers

mix of different market mediators of the conveyance channel,

which diminishes in general cost; in this manner further

driving interest for this portion.

Regional Insights

The North America showcase represented the biggest offer

in 2016 and is relied upon to keep up its situation during the

figure time frame. This generous offer can be ascribed to

exceptional change in way of life, bringing about more

noteworthy occurrence of gastrointestinal sicknesses.

Besides, nearness of government activities planned for

forestalling just as treating gastrointestinal infections is

required to drive the market. For example, the Integrated

Global Action Plan for Diarrhea by UNICEF and WHO targets

limiting preventable youth passing’s because of loose bowels

by giving intercessions and administrations to bring issues to

light and give access to treatment and preventive measures.

Asia Pacific is foreseen to show exponential development all

through the estimate time frame. This is probably going to be

energized by predictable endeavors attempted by key players,

which incorporate R&D speculations just as commercialization

of marked medications at a moderately lower cost.

Furthermore, critical need to control high frequency pace of

gastrointestinal issue and innovative up gradation of human

services framework are anticipated to give the local market

high potential development openings over the gauge time

frame.

A portion of the key players in the market are Takeda

Pharmaceuticals, Valeant Pharmaceuticals, Allergan plc. and

Bayer AG. These key players have broadly utilized challenge

maintainability methodologies, for example, new item

improvement and provincial and circulation channel extension

to increase a higher offer in the market. Besides, expanded

spotlight on refining activity and store network the executives

has encouraged key players to keep up an aggressive edge.

For example, in October 2016, Allergan plc. finished a

divesture of its generics business by selling Anda, Inc. to Teva

Pharmaceuticals Industries Ltd. This divesture was completed

to build the organization's attention on marked

pharmaceuticals and extend key therapeutics zones.

Essentially, in January 2016, Takeda Pharmaceuticals went into

vital coordinated effort with Cour Pharmaceutical

Development to create propelled therapeutics for a wide

scope of gastrointestinal infections.

Report Scope

Table

Attribute

Details

Base year for estimation

2016

Actual estimates/Historical data

2014 - 2016

Forecast period

2017 - 2025

Market representation

Revenue in USD Million and CAGR from 2017 to 2025

Regional scope

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Country scope

U.S., Canada, Germany, U.K., Japan, China, India, Brazil, Mexico, South Africa

Report coverage

Revenue forecast, company share, competitive landscape, growth factors and trends

15% free customization scope (equivalent to 5 analyst working days)

If you need specific market information, which is not currently within the scope of the report, we will provide it to you as a part of customization

Segments Covered in the Report

This report gauges income development at worldwide,

territorial, and nation levels and gives an examination on most

recent industry drifts in every one of the sub-fragments from

2014 to 2025. With the end goal of this examination, Grand

View Research has sectioned the worldwide gastrointestinal

therapeutics advertise based on type, course of organization,

application, dispersion channel, and locale:

• Type Outlook (Revenue, USD Million, 2014 - 2025)

• Branded

• Aminosalicylates

• Antacids

• Enzyme Replacement Therapies

• Proton-siphon Inhibitors

• Laxatives

• Antiemetics

• H2 Antagonists

• Antidiarrheals

• Biologics

• Others

• Generics

• Route of Administration Outlook (Revenue, USD Million, 2014 - 2025)

• Oral

• Intravenous

• Others

• Application Outlook (Revenue, USD Million, 2014 - 2025)

• Ulcerative Colitis

• Crohn's Disease

• GERD

• Others

• Distribution Channel Outlook (Revenue, USD Million, 2014 - 2025)

• Hospital Pharmacies

• Retail Pharmacies

• Online Pharmacies

• Regional Outlook (Revenue, USD Million, 2014 - 2025)